Definition.

Economic capital can be defined as capital needed against unexpected future losses at a given confidence level for a certain time horizon. Thus, Economic capital is a forward-looking measure of capital adequacy based on a probabilistic assessment of potential future losses.

Economic capital is a measure of risk, not of capital held. So, it is different and distinct from accounting and regulatory capital measures. The output of economic capital models also differs from many other measures of capital adequacy. Model results are expressed as a dollar level of capital necessary to adequately support specific risks assumed. Whereas most traditional measures of capital adequacy relate existing capital levels to assets or some form of adjusted assets, economic capital relates capital to risks, regardless of the existence of assets. The development and implementation of a well-functioning economic capital model can make bank management better equipped to anticipate potential problems. Conceptually, economic capital can be expressed as protection against unexpected future losses at a selected confidence level. Most banks calculate economic capital on a monthly or quarterly basis.

Economic Capital can also be defined as the difference between some given percentile of a loss distribution and the expected loss. It is sometimes referred to as “unexpected loss at the confidence level.”

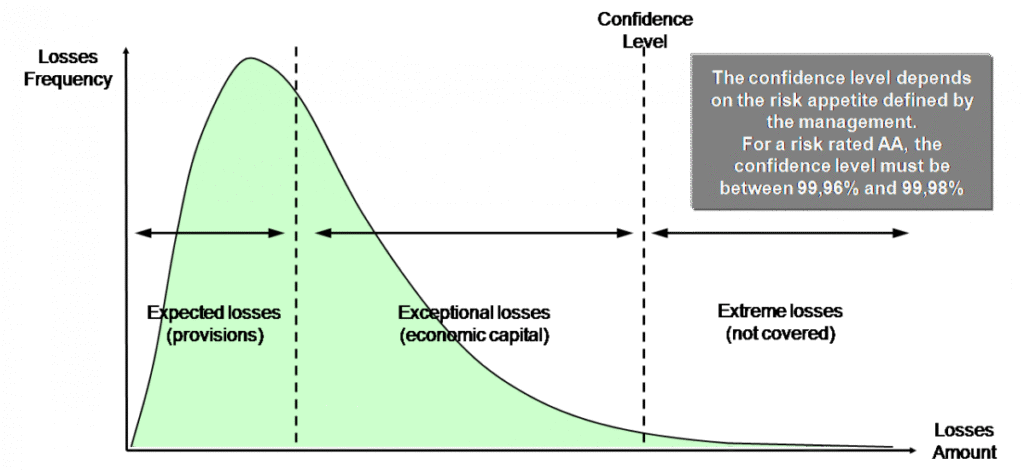

The economic capital aims only at covering unexpected losses (exceptional losses). Expected losses should be covered by provisions, while extreme losses are not covered under this approach.

The confidence level is established by bank and can be viewed as the risk of insolvency during a defined time period at which Bank has chosen to operate. The higher the confidence level selected, the lower the probability of insolvency. For example, if Bank establishes a 99.97 percent confidence level, that means it is accepting a 3 in 10,000 probability of the bank becoming insolvent during the next twelve months. Many banks using economic capital models select a confidence level between 99.96 and 99.98 percent, equivalent to the insolvency rate expected for an AA or Aa credit rating.

Shareholder Value Added (SVA), is a dollar measure of performance.

SVA= Economic Net Income – (Economic Capital at Risk * Hurdle Rate)

Several other definitions of Economic Capital are :

Sufficient surplus to meet potential negative cash flows and reductions in value of assets or increase in value of liabilities at a given level of risk tolerance, over a specified time horizon.

Excess of the market value of the assets over the fair value of liabilities required to ensure that obligations can be satisfied at a given level of risk tolerance, over a specified time horizon.

Sufficient surplus to maintain solvency at a given level of risk tolerance, over a specified time horizon.

Economic capital differs from the minimum regulatory capital requirement because a financial institution may include risks that are not formally subject to the minimum regulatory capital (e.g. liquidity risk, reputational risk, business risk or interest rate risk in the banking book) or may use different parameters or methodologies for credit risk, market risk or operational risk.

Adoption of Economic Capital contributes to a more comprehensive pricing system that covers expected and unexpected losses, assist in the evaluation of the adequacy of capital in relation to the bank’s overall risk profile, develop risk-adjusted performance measures that provide for better evaluation of returns and the volatility of returns and enhance risk management efforts by providing a common currency for risk.

Expected loss is the anticipated average loss over a defined period of time. Expected losses represent a cost of doing business and are generally expected to be absorbed by operating income. In the case of loan losses, for example, the expected loss should be priced into the yield and an appropriate charge included in the allowance for loan and lease losses.

Expected losses ($) = PD(%) * LGD(%) * EAD($)

Banks may also calculate EL by taking into consideration stressed Risk Measures. In that case,

Expected losses ($) = SPD(%) * SLGD(%) * SEAD($)

Unexpected Loss is the potential for actual loss to exceed the expected loss and is a measure of the uncertainty inherent in the loss estimate. It is this possibility for unexpected losses to occur that necessitates the holding of capital protection.

Calculation Methodology

There is no standard methodology for calculating Economic Risk Capital. Some of the leading Banks of Middle East calculate it as given below:

Economic Risk Capital = [ Credit Risk Capital + Ops Risk Capital+ Counterparty Credit Risk Capital +CVA Capital Charge]

Some of the leading Banks in Europe calculate it as given below:

Economic Risk Capital = [ Position Risk Capital + Operational Risk Capital+ Other Risk Capital + Expense Risk Capital + Model Add On Capital ]

Position Risk Capital = The level of Unexpected Loss in economic value of the portfolio of positions over 1 Year holding period at 99.97% confidence level. It involves the following risks:

(a) Trading Risk of Foreign Exchange rates and volatilities; Interest Rate levels and volatilities; Equity Prices and volatilities; Commodity Prices and volatilities.

(b) Equity Arbitrage Risk activities, like mergers and acquisitions not done as announced earlier.

(c) Liquid Hedge Fund Risk

(d) Insurance Risk associated with life financing and litigation.

(e) Rsidential Real Estate and ABS Risk

(f) Non Recourse Share Backed Financing Risk

(g) Traded Credit Risk

(h) Coorelation Risk between different market factors, assets and risk types

(i) International Lending and Counterparty Risk

(j) Private Banking Lending Risk

(k) Illiquid Investment Risk

(l) Emerging Country Event Risk

(m) Commercial Real Estste Risk

Operational Risk Capital = The loss resulting from inadequate or failed internal processes, people and systems or from external events over 1 Year holding period at 99.97% confidence level. It includes:

(a) Failed settlements, documentation and reporting errors

(b) Internal or external fraud

(c) Unauthorized trading activity

(d) Improper business and market practices

(e) Lack of fiduciary duty

(f) Technology breakdown

(g) Unavailability of building

It should also include Reputational Risk and Strategy Risk wherever possible.

Expense Risk Capital = (Stressed Expenses – Stressed Revenue) in an ERC event.

It takes into account the following:

(a) Trading Income in crash

(b) Commission & Fees in crash

(c) Net Interest Income in crash

(d) Advisory in crash

(e) Underwriting in crash

(f) Management Fees in crash

(g) Performance Fees in crash

(h) Private Equity Commission in crash

(i) Private Equity Investment Gains in crash

(j) Other Income in crash

(k) Expenses in crash

Other Risk Capital = Foreign Exchange Translation Risk not captured by Position Risk on a Currency + Corporate Interest Rate Risk on strategic equity exposures + Owned Real Estate Risk + Employee Pension Fund Valuation Risk + Employee Deferred Equity Compensation Benefit Risk

Other Risk Capital is calculated at 99.97% Confidence Level for 1 Year holding period.

Model Add On Capital = Risks not captured in ERC + Risks due to planned methodology changes + Risk for general Model uncertainty.

Uses of Economic Capital

- Business Unit level use: The effective use of economic capital at the business-unit level depends on how relevant the economic capital allocated to or absorbed by a business unit is with respect to the decision-making processes that take place within it. Frequently, the success or failure of an economic capital framework in a bank can be assessed by looking at how business line managers perceive the constraints imposed and the opportunities offered by economic capital in the following areas: (i) credit portfolio management (ii) risk-based pricing (iii) customer profitability analysis (iv) customer segmentation (v) portfolio optimisation (vi) management incentives in internal decision-making processes.

- Enterprise-wide or Group-level use: Economic capital provides banks with a common currency for measuring, monitoring, and controlling: (i) different risk types (ii) the risks of different business units. The risk types that are typically covered by banks’ economic capital models are credit risk, market risk, interest rate risk in the banking book –(IRRBB) and operational risk. Concentration risk as part of credit risk is taken care of. Other risks included are business/strategic risk, counterparty credit risk, insurance risk, real estate risk and model risk.

In order to assess relative performance on a risk-adjusted basis, banks calculate risk adjusted performance measures, where economic capital measures play an important role. The most commonly used risk-adjusted performance measures are risk-adjusted return on capital (RAROC) and shareholder value added (SVA). Many banks calculate these measures at various levels of the enterprise (Entity level, Business Unit level and Portfolio level). The major difference between these two measures is that RAROC is a relative measure, while SVA is an absolute measure. RAROC provides information which is useful in comparing the performances of two portfolios with the same amount of economic net income, but with substantially different economic capital measures. One of the key issues in using both RAROC and SVA for performance measurement is how to set the Hurdle Rate that reflects the bank’s cost of capital. In this regard practices vary across banks. Some banks set a single cost of capital (weighted average cost of capital or target return on equity – ROE) across all business units, while other banks set required returns that vary according to the risks of the business units.

There are other risk-adjusted performance measures that could be used. Some of these measures include:

RORAC = (return on risk-adjusted capital),

ROCAR = (return on capital at risk)

RAROA = (risk-adjusted return on assets).

Difference Between Economic Capital and Regulatory Capital

For economic capital, the primary stakeholders are the bank’s shareholders, and the objective is the maximization of their wealth. The objective of bank directors is to maximize the return to their shareholders, by maximizing the profits generated by the bank’s activities through the optimal allocation of capital across different business lines.

For regulatory capital, the primary stakeholders are the bank’s depositors and the objective is to minimize the possibility of loss. The ultimate objectives of supervisors are to protect depositors, ensure the soundness of financial institutions and prevent financial crises.

Economic Capital is calculated internally by Banks and FIs and it can be less or more than regulatory capital whereas Regulatory Capital is calculated as per the regulation.

Top-Down Approach: The economic capital can be calculated using the aggregate performance information at the enterprise level, using Earnings Volatility Approach or Black-Scholes Approach for Stock Prices.

Bottom-Up Approach: The economic capital is estimated by modelling individual transactions and business units and then aggregating the risk using statistical models. This approach is preferred over top-down approaches because of the high level of transparency and the ability to segregate credit risk, market risk, and operational risk.

IMPORTANCE OF ECONOMIC CAPITAL

Economic Capital plays a vital role in the financial management of the Bank and Fis.

Solvency and Capital Efficiency: Economic Capital Analysis enables to strike an appropriate balance between

• Too much capital – which can lead to an excessive cost of funding

• Not enough capital – which can lead to an unacceptable risk of insolvency

Risk Monitoring and Control: EC is a key component of risk appetite frame work. The risk measurement and monitoring processes need to ensure that the business operation remains within that risk appetite. To do this, target ranges for EC utilization need to be established for each geography, business unit and/or risk and actual EC utilisation be monitored against these target ranges.

Performance Measurement and Management: By itself, EC does not represent a measure of business performance, but it provides a measure of the risk related to the business. For example, a higher level of EC for one business unit compared to another signifies a higher level of risk and therefore suggests that a higher level of reward should be expected. Therefore, to use EC as a performance metric, it needs to be incorporated with some risk related measure of return, like RAROC and then calculate RAROC for each business unit, using EC as the (risk adjusted) capital measure in the denominator of the calculations.

Risk Based Decision Making: EC can be incorporated in the key risk- based decision processes such as

strategic asset allocation, ALM and Banking and reinsurance strategy. The impact of such decisions on the company’s EC requirement needs to be assessed before embarking on a particular course of action.

Risk Based Pricing: With the EC framework becoming more mature and relevant, EC is being used for product pricing.

Business Planning: It will be important to assess the impact of alternative business plans (alternative product mixes and volumes) on the overall EC requirement of the banks, FIs and insurance companies. For example, business plans/strategies involving a wide range of products can provide higher diversification benefits and hence lower unit economic capital requirements.

Mergers and Acquisitions: EC can play an important role in the merger and acquisition process. The

buyer will need to consider the EC requirements of the target company and the result of aggregating these with its own EC requirements, taking into account diversification where necessary.

ERC Ratios

Available Economic Capital (AEC) is the capital net of adjustments required to provide consistency with ERC. It represents the bridge between the economic based ERC and the accounting based capital measures and helps in meaningful comparison between capital needs and capital resources.

AEC = Tier I Capital + Other Comprehensive Income + Unrealized Capital Gains + Unrealized Gains on Owned Real Estate + Adjustments on Own Shares, Goodwill and securitization exposures + Accrued/Proposed Dividend – Minimum Dividend(in a crisis situation).

ERC Coverage Ratio provides a reference point for a structured assessment of the Group’s solvency as a whole. It can also be used as a key metric for the internal capital adequacy assessment process (ICAAP) which will help in best internal assessment of risk and loss absorbing capacity of the Bank.

ERC Coverage Ratio = Available Economic Capital / Total ERC

Higher the ERC Coverage Ratio, better it is for the firm.