What is Liquidity Risk

- Liquidity is a financial institution’s capacity to meet its cash and collateral obligations without incurring unacceptable losses. Adequate liquidity is dependent upon the institution’s ability to efficiently meet both expected and unexpected cash flows and collateral needs without adversely affecting either daily operations or the financial condition of the institution.

- Liquidity risk is the risk to an institution’s financial condition or safety and soundness arising from its inability (whether real or perceived) to meet its contractual obligations. The primary role of liquidity-risk management is to (1) prospectively assess the need for funds to meet obligations and (2) ensure the availability of cash or collateral to fulfill those needs at the appropriate time by coordinating the various sources of funds available to the institution under normal and stressed conditions.

Impact of Liquidity Losses

The United Kingdom experienced its first bank run in over 140 years. In September 2007, television viewers around the world witnessed the spectacle of what seemed like an old-fashioned bank run – of depositors waiting in line outside the branch offices of the UK bank, Northern Rock, a significant retail bank and a substantial mortgage lender , to withdraw their money.

The last bank run in the UK before Northern Rock was in 1866 (with Overend & Guerney). Runs were more common in the US in the 1930s, but they have been rare since.

Retail depositors started queuing outside the branch offices only after the Bank of England announced its emergency liquidity support for Northern Rock on the morning of Friday, September 14th. On the previous evening the BBC’s evening television news broadcast first broke the news that Northern Rock had

sought the Bank of England’s support.

Around £3 billion of deposits were withdrawn (around 11 percent of the bank’s total retail deposits) from Northern Rock (NR) in a span of 3 days only.

Types of Liquidity in Banks

Central Bank Liquidity: Central bank liquidity is the ability of the central bank to supply the liquidity needed to the financial system. It is typically measured as the liquidity supplied to the economy by the central bank. It relates to central bank operations liquidity which refers to the amount of liquidity provided through the central bank auctions to the money market according to the monetary policy stance. The need for banknotes and the obligations of banks to fulfill the reserve requirements create an aggregate liquidity deficit in the system, thereby making it reliant on refinancing from the central bank. The central bank, being the monopoly provider of the monetary base, provides liquidity to the financial system through its open market operations (OMO).

Funding Liquidity: The Basel Committee of Banking supervision defines funding liquidity as the ability of banks to meet their liabilities, unwind or settle their positions as they come due (BIS, 2008)11. Similarly, the IMF provides a definition of funding liquidity as the ability of solvent institutions to make agreed upon payments in a timely fashion. A bank can always go to the asset market and sell its assets or generate liquidity through securitization, loan syndication and the secondary market for loans, in its role as an originator and distributor. Moreover, the bank can get liquidity from the interbank market, arguably the most important source of liquidity. Finally, a bank can also choose to get funding liquidity directly from the central bank.

Market Liquidity: Market liquidity is the ability to trade an asset at short notice, at low cost and with little impact on its price.

Liquidity Risk in Banks

All the three distinct types of liquidity are intensively interconnected.

| Liquidity Type | Role |

| Central Bank Liquidity | Provision of amount of liquidity that balances demand & supply |

| Market Liquidity | Redistribution and Recycling of liquidity |

| Funding Liquidity | Efficient allocation & optimum utilization of liquidity resources |

Central Bank Liquidity Risk does not exist in developed, industrialised countries, in theory, as the central bank is always able to supply base money and, therefore, can never be illiquid because it is the originator of the monetary base and can dispense liquidity as and when deemed necessary.

Market Liquidity Risk very much exists for Banks and can be defined as the risk that a given security or asset cannot be sold quickly enough in the market to prevent a loss. In such circumstances, Bank may be unable to meet short term financial demands. This usually occurs due to the inability to convert a security or hard asset to cash without incurring a loss of capital. It is the systematic, non-diversifiable component of liquidity risk.

Funding Liquidity Risk very much exists for Banks. It has been found that Banks are unable to meet their contractual obligations when they become due.

Liquidity Coverage Ratio (LCR)

The financial crisis of 2007 highlighted significant lapses in liquidity management among banks, despite adequate capital levels. This led to the development of the LCR as a response to ensure better liquidity risk management.

- Many banks faced liquidity issues during the financial crisis of 2007 due to poor management practices.

- The crisis underscored the importance of liquidity in maintaining the stability of financial markets.

- The Basel Committee published the “Sound Principles” in 2008 to guide banks in liquidity risk management.

The Liquidity Coverage Ratio (LCR) is a key reform by the Basel Committee aimed at enhancing the short-term resilience of banks’ liquidity risk profiles. It ensures that banks maintain an adequate stock of high-quality liquid assets (HQLA) to meet liquidity needs during a 30-day stress scenario. By then, it is assumed that appropriate corrective action can be taken by management and supervisors, or that the bank can be resolved in an orderly way.

- The LCR requires banks to hold sufficient HQLA to cover total net cash outflows for 30 days.

- The minimum LCR requirement is set at 100%, meaning HQLA must equal or exceed net cash outflows.

- The LCR aims to reduce the risk of financial spillover to the real economy during stress events.

LCR is defined as stock of unencumbered high-quality liquid assets (HQLA) that can be easily and immediately converted into cash in private markets with little or no loss of value to meet their liquidity needs for a 30calendar days under liquidity stress scenario, arising from financial & economic stress.

Stock of Unencumbered High Quality Liquid Assets (HQLA)

LCR = —————————————————————————————- ≥ 100%

Net Cash Outflow Over 30 Calendar Days

The formula for the calculation of the stock of HQLA is as follows:

Stock of HQLA = Level 1 + Level 2A + Level 2B – Adjustment for 15% cap – Adjustment for 40% cap

Where:

Adjustment for 15% cap = Max (Adjusted Level 2B – 15/85*(Adjusted Level 1 + Adjusted Level 2A), Adjusted Level 2B – 15/60*Adjusted Level 1, 0)

Adjustment for 40% cap = Max ((Adjusted Level 2A + Adjusted Level 2B – Adjustment for 15% cap) – 2/3*Adjusted Level 1 assets, 0)

Alternatively, the formula can be expressed as:

Stock of HQLA = Level 1 + Level 2A + Level 2B – Max ((Adjusted Level 2A+Adjusted Level 2B) – 2/3*Adjusted Level 1, Adjusted Level 2B – 15/85*(Adjusted Level 1 + Adjusted Level 2A), 0)

Total net cash outflows over the next 30 calendar days = Total expected cash outflows – Min{total expected cash inflows; 75% of total expected cash outflows}

LCR must be reported at least Monthly, with potential for more frequent reporting in stress situations like Weekly or Daily. The LCR must be monitored in significant currencies to capture potential mismatches. Significant currencies are those with liabilities amounting to 5% or more of total liabilities. The LCR is required to be met in one single currency, but monitoring in significant currencies is essential.

Banks must ensure that the excess of outflows over inflows over a rolling 30day calendar period does not exceed the amount of high-quality liquid assets available to the bank. These liquid assets cover cash, qualifying marketable securities from sovereigns, central banks, PSEs, multilateral development banks as well as other high-quality public and corporate debt and common equity shares. In the absence of any financial stress, LCR has to be 100%. However, during a period of financial & liquidity stress, Banks are allowed to have a lower LCR, thereby falling below 100% and banks can use their stock of HQLA which is intended to serve as a defense against the potential onset of liquidity stress.

The LCR was introduced gradually from 1 January 2015 but the minimum requirement was set at 60% and rose by 10% every year to reach 100% on 1 January 2019. This graduated approach was adopted to ensure no material disruption to the orderly strengthening of banking systems or the ongoing financing of economic activity.

Unencumbered Assets: Unencumbered Assets are those assets which are free of legal, regulatory, contractual or other restrictions on the ability of the bank to liquidate, sell, transfer, or assign the asset.

HQLA in a Nutshell

Characteristics and Requirements of HQLA

HQLA must be easily convertible to cash with minimal loss in value and include low risk, ease of valuation, and market-related factors.

- HQLA should be low-risk assets with high credit standing and low correlation with risky assets.

- Assets must be liquid in stressed conditions and ideally eligible for central bank use.

- Operational requirements ensure that HQLA can be monetized quickly during stress periods.

Diversification and Management of HQLA

The stock of HQLA should be diversified across asset classes to mitigate risks associated with market shocks. Banks must have policies to avoid concentration in specific asset types or issuers.

- Diversification is crucial to ensure liquidity remains intact during severe market stress.

- Banks should monitor and manage their HQLA to ensure they can meet liquidity needs effectively.

- The LCR must be reported in a single currency, but banks should also manage liquidity in each currency.

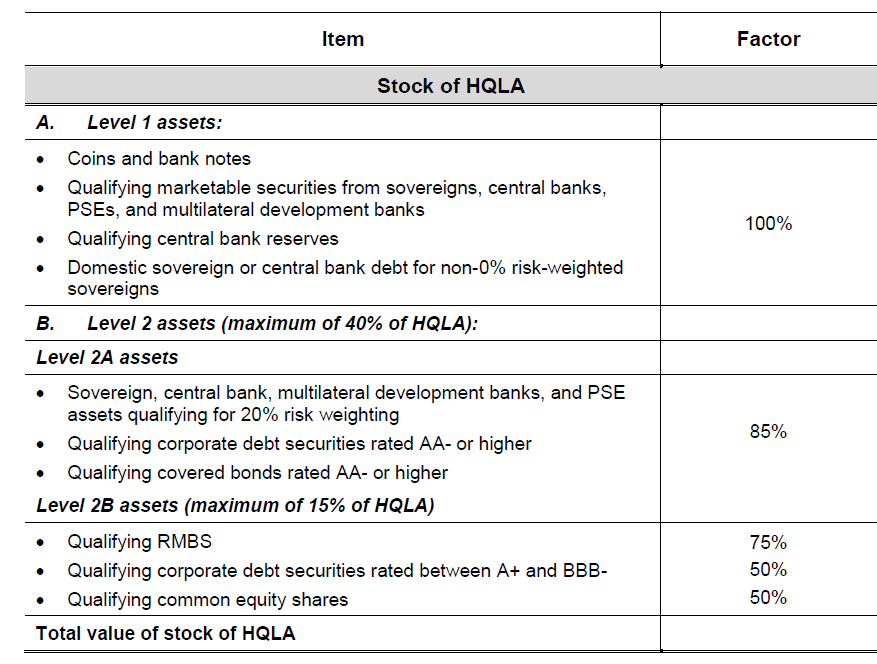

HQLA: consists of Level 1, Level 2A and Level 2B Assets.

Level 1 assets can be included without limit, while Level 2 assets are capped at 40% of the total stock. Level 2B assets, if included, must not exceed 15% of the total HQLA stock. The calculation of caps considers required haircuts and short-term transactions.

Level 1 Assets Characteristics

Level 1 assets are the highest quality liquid assets that can be included in the HQLA stock without any haircut. They are essential for banks to meet liquidity requirements.

(a) coins and banknotes;

(b) central bank reserves (including required reserves), to the extent that the central bank policies allow them to be drawn down in times of stress. Central bank reserves include banks’ overnight deposits with the central bank, and term deposits with the central bank that:(i) are explicitly and contractually repayable on notice from the depositing bank; or (ii) that constitute a loan against which the bank can borrow on a term basis or on an overnight but automatically renewable basis (only where the bank has an existing deposit with the relevant central bank). Other term deposits with central banks are not eligible for the stock of HQLA.

(c) marketable securities representing claims on or guaranteed by sovereigns, central banks, PSEs, the Bank for International Settlements, the International Monetary Fund, the European Central Bank and European Community, or multilateral development banks and satisfying all of the following conditions:

• assigned a 0% risk-weight under the Basel II Standardised Approach for credit risk.

• traded in large, deep and active repo or cash markets characterised by a low level of concentration.

• have a proven record as a reliable source of liquidity in the markets (repo or sale) even during stressed market conditions.

• not an obligation of a financial institution or any of its affiliated entities.

(d) where the sovereign has a non-0% risk weight, sovereign or central bank debt securities issued in domestic currencies by the sovereign or central bank in the country in which the liquidity risk is being taken or in the bank’s home country.

(e) where the sovereign has a non-0% risk weight, domestic sovereign or central bank debt securities issued in foreign currencies are eligible up to the amount of the bank’s stressed net cash outflows in that specific foreign currency stemming from the bank’s operations in the jurisdiction where the bank’s liquidity risk is being taken.

Level 2 Assets Classification- Level 2A and Level 2B

Level 2A Assets

A 15% haircut is applied to the current market value of each Level 2A asset held in the stock of HQLA. Level 2A assets are limited to the following:

(a) Marketable securities representing claims on or guaranteed by sovereigns, central banks, PSEs or multilateral development banks that satisfy all of the following conditions:

• assigned a 20% risk weight under the Basel II Standardised Approach for credit risk.

• traded in large, deep and active repo or cash markets characterised by a low level of concentration.

• have a proven record as a reliable source of liquidity in the markets (repo or sale) even during stressed market conditions (ie maximum decline of price not exceeding 10% or increase in haircut not exceeding 10 percentage points over a 30-day period during a relevant period of significant liquidity stress).

• not an obligation of a financial institution or any of its affiliated entities.

(b) Corporate debt securities (including commercial paper) and covered bonds that satisfy all of the following conditions:

• in the case of corporate debt securities: not issued by a financial institution or any of its affiliated entities.

• in the case of covered bonds: not issued by the bank itself or any of its affiliated entities.

either (i) have a long-term credit rating from a recognised external credit assessment institution (ECAI) of at least AA or in the absence of a long-term rating, a short-term rating equivalent in quality to the long-term rating or (ii) do not have a credit assessment by a recognised ECAI but are internally rated as having a probability of default (PD) corresponding to a credit rating of at least AA-.

• traded in large, deep and active repo or cash markets characterised by a low level of concentration.

• have a proven record as a reliable source of liquidity in the markets (repo or sale) even during stressed market conditions: ie maximum decline of price or increase in haircut over a 30-day period during a relevant period of significant liquidity stress not exceeding 10%.

Level 2B Assets

A larger haircut is applied to the current market value of each Level 2B assets held in the stock of HQLA. Level 2B assets are limited to the following:

(a) Residential mortgage backed securities (RMBS) that satisfy all of the following conditions are included in Level 2B, subject to a 25% haircut:

• not issued by and the underlying assets have not been originated by the bank itself or any of its affiliated entities.

• have a long-term credit rating from a recognised ECAI of AA or higher, or in the absence of a long-term rating, a short-term rating equivalent in quality to the long-term rating.

• traded in large, deep and active repo or cash markets characterised by a low level of concentration.

• have a proven record as a reliable source of liquidity in the markets (repo or sale) even during stressed market conditions, ie a maximum decline of price not exceeding 20% or increase in haircut over a 30-day period not exceeding 20 percentage points during a relevant period of significant liquidity stress.

• the underlying asset pool is restricted to residential mortgages and cannot contain structured products.

• the underlying mortgages are “full recourse’’ loans (in the case of foreclosure the mortgage owner remains liable for any shortfall in sales proceeds from the property) and have a maximum loan-to-value ratio (LTV) of 80% on average at issuance.

• the securitisations are subject to “risk retention” regulations which require issuers to retain an interest in the assets they securitise.

(b) Corporate debt securities (including commercial paper) that satisfy all of the following conditions are included in Level 2B, subject to a 50% haircut:

• not issued by a financial institution or any of its affiliated entities.

• either (i) have a long-term credit rating from a recognised ECAI between A+ and BBB- or in the absence of a long term rating, a short-term rating equivalent in quality to the long-term rating; or (ii) do not have a credit assessment by a recognised ECAI and are internally rated as having a PD corresponding to a credit rating of between A+ and BBB-.

• traded in large, deep and active repo or cash markets characterised by a low level of concentration.

• have a proven record as a reliable source of liquidity in the markets (repo or sale) even during stressed market conditions, ie a maximum decline of price not exceeding 20% or increase in haircut over a 30-day period not exceeding 20 percentage points during a relevant period of significant liquidity stress.

(c) Common equity shares that satisfy all of the following conditions may be included in Level 2B, subject to a 50% haircut:

• not issued by a financial institution or any of its affiliated entities.

• exchange traded and centrally cleared.

• a constituent of the major stock index in the home jurisdiction or where the liquidity risk is taken, as decided by the supervisor in the jurisdiction where the index is located.

• denominated in the domestic currency of a bank’s home jurisdiction or in the currency of the jurisdiction where a bank’s liquidity risk is taken.

• traded in large, deep and active repo or cash markets characterised by a low level of concentration.

• have a proven record as a reliable source of liquidity in the markets (repo or sale) even during stressed market conditions, ie a maximum decline of share price not exceeding 40% or increase in haircut not exceeding 40 percentage points over a 30-day period during a relevant period of significant liquidity.

Alternative Liquidity Approaches for Insufficient HQLA

Jurisdictions with insufficient HQLA may adopt alternative liquidity approaches (ALA) to address liquidity needs. These approaches are subject to specific criteria and supervisory oversight.

- Jurisdictions must demonstrate a structural shortfall in HQLA.

- Options include accessing central bank liquidity facilities or using foreign currency HQLA to cover domestic liquidity needs.

- A maximum usage limit for these options must be established by supervisors.

Supervisors must monitor and disclose the use of these alternative treatments.

Some jurisdictions may have an insufficient supply of Level 1 assets (or both Level 1 and Level 2 assets) in their domestic currency to meet the aggregate demand of banks. To address this situation, the Committee has developed alternative treatments for holdings in the stock of HQLA, which are expected to apply to a limited number of currencies and jurisdictions. To qualify for the alternative treatment, a jurisdiction should be able to demonstrate that:

• there is an insufficient supply of HQLA in its domestic currency, taking into account all relevant factors affecting the supply of, and demand for, such HQLA.

• the insufficiency is caused by long-term structural constraints that cannot be resolved within the medium term.

• it has the capacity, through any mechanism or control in place, to limit or mitigate the risk that the alternative treatment cannot work as expected.

• it is committed to observing the obligations relating to supervisory monitoring, disclosure, and periodic self-assessment and independent peer review of its eligibility for alternative treatment.

All of the above criteria have to be met to qualify for the alternative treatment.

Liquidity Risk Monitoring Tools

The following metrics capture specific information related to a bank’s cash flows, balance sheet structure, available unencumbered collateral and certain market indicators.

I. Contractual maturity mismatch– identifies the gaps between the contractual inflows and outflows of liquidity from all on- and off-balance sheet items for defined time bands. These maturity gaps indicate how much liquidity a bank would potentially need to raise in each of these time bands if all outflows occurred at the earliest possible date.

II. Concentration of funding– identifies those sources of wholesale funding that are of such significance that withdrawal of this funding could trigger liquidity problem.

A. Funding liabilities sourced from each significant counterparty as a % of total liabilities

B. Funding liabilities sourced from each significant product/instrument as a % of total liabilities

C. List of asset and liability amounts by significant currency

III. Available unencumbered assets– provides supervisors with data on the quantity and key characteristics, including currency denomination and location of banks’ available unencumbered assets. These assets have the potential to be used as collateral to raise additional HQLA or secured funding in secondary markets or are eligible at central banks and as such may potentially be additional sources of liquidity for the bank.

A. Available unencumbered assets that are marketable as collateral in secondary markets

B. Available unencumbered assets that are eligible for central banks’ standing facilities

IV. LCR by significant currency– While the LCR is required to be met in one single currency, in order to better capture potential currency mismatches, banks and supervisors should also monitor the LCR in significant currencies. This will allow the bank and the supervisor to track potential currency mismatches that could arise and take corrective actions.

Foreign Currency LCR = Stock of HQLA in each significant currency / Total net cash outflows over a 30-day time period in each significant currency

(Amount of total net foreign exchange cash outflows should be net of foreign exchange hedges)

Net Stable Funding Ratio (NSFR)

Net Stable Funding Ratio (NSFR): The Net Stable Funding Ratio complements the LCR and focuses on the medium and long term source

of funding for banks. NSFR is defined as:

Available amount of Stable Funding

Net Stable Funding Ratio = ———————————————– ≥ 100%

Required amount of Stable Funding

Introduction 1 January 2018

Scope of Application Individual Bank-specific

Reporting Quarterly

Disclosure Disclosure of NSFR under Pillar 3

The NSFR requirement means that illiquid loans to customers, with maturities of 12 months or more, need to be matched with funding from internal or external sources with a similar maturity rather than by short term inter-bank lending.

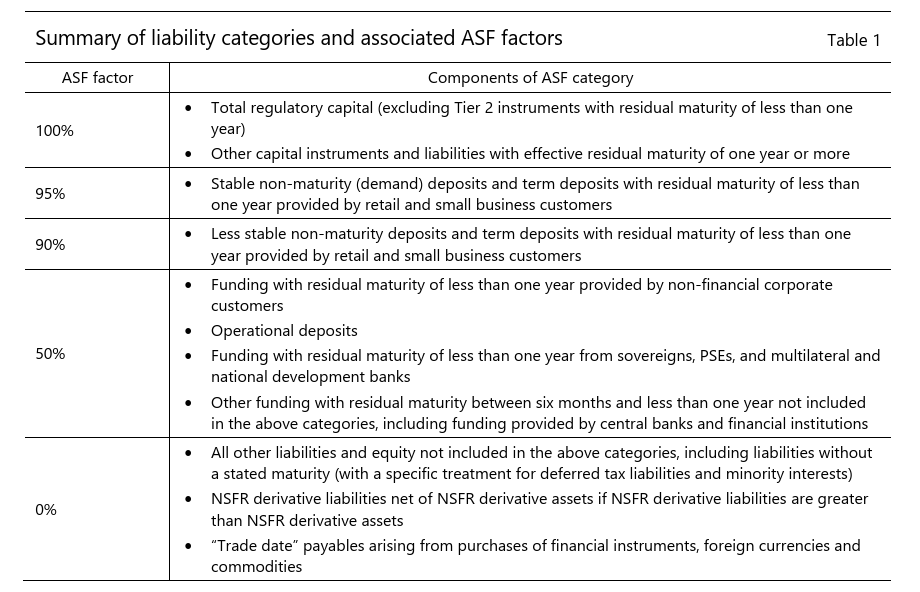

Available amount of Stable Funding (ASF) refers to the reliability of the sources of funding over a one-year horizon.

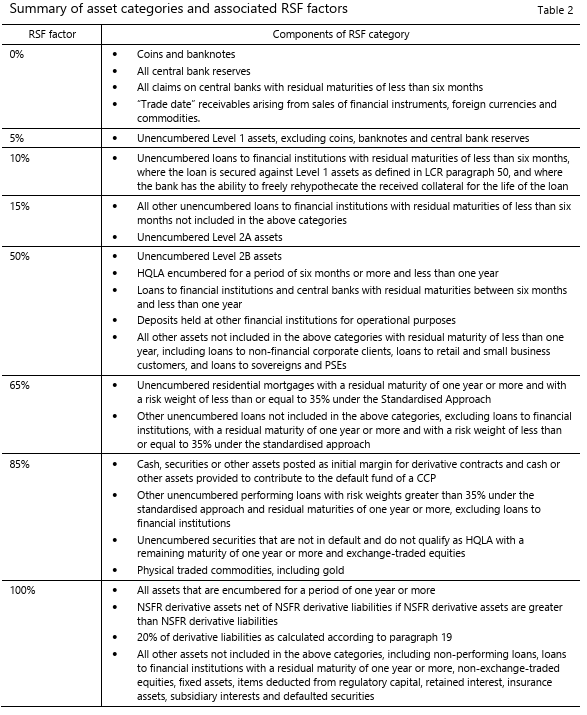

Required amount of Stable Funding (RSF) refers to the value of assets that require funding. The precise calculations for both ASF and RSF are weighted to reflect the degree of stability of existing liabilities (under ASF) and the level of support a supervisor believes an asset requires (under RSF).

Furthermore, these calculations are subject to a stressed scenario: A significant decline in profitability or solvency arising from heightened credit risk, market risk or operational risk and/ or other risk exposures and/or A potential downgrade in a debt, counterparty credit or deposit rating by any nationally recognized credit rating organization and/or A material event that calls into question the reputation or credit quality of the institution.

ASF = 0% x MAX ((NSFR derivative liabilities – NSFR derivative assets), 0).

ASF categories and the associated maximum ASF factor to be applied in calculating an institution’s total amount of available stable funding under the standard is given in Table 1.

Table 2 summarises the specific types of assets to be assigned to each asset category and their associated RSF factor.

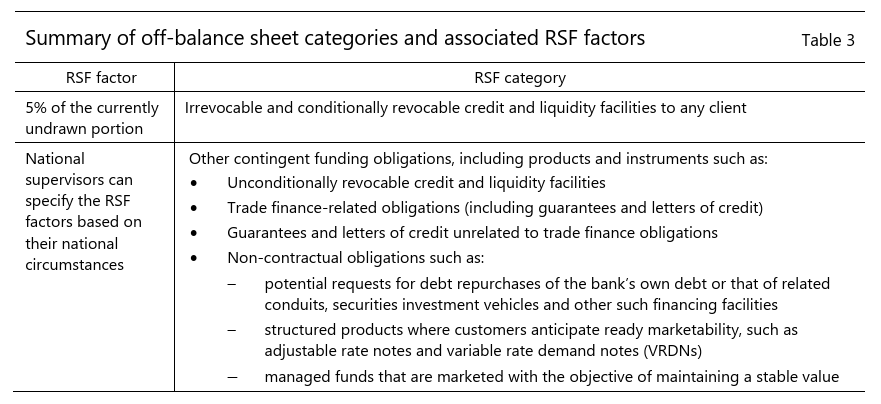

NSFR identifies OBS exposure categories based broadly on whether the commitment is a credit or liquidity facility or some other contingent funding obligation.

Stress Testing and Scenario Framework

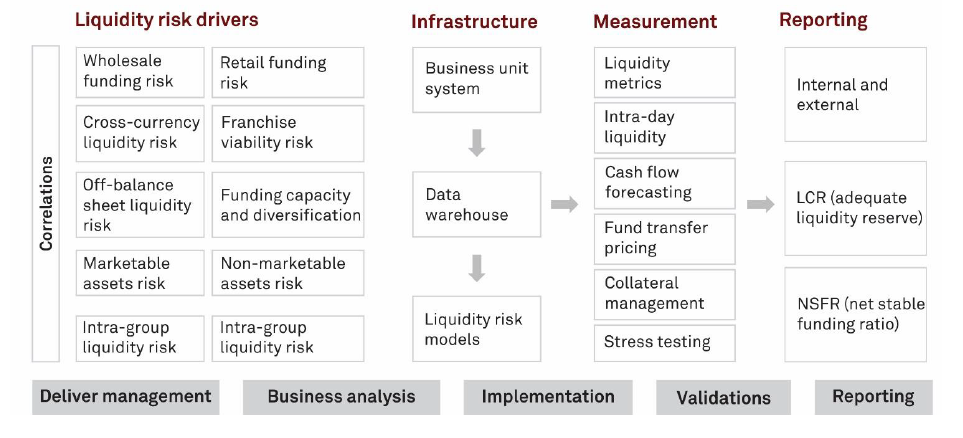

Liquidty Risk Framework

Testing Techniques

The liquidity stress test involves three approaches, namely historical statistical techniques, deterministic models, and Monte Carlo simulation.

•Historical statistical approach: This stress testing technique models an institution’s historical pro forma cash flow subject to the observed cash flow volatility of the institution. An example is the cash flow at risk approach (CFaR).

•Deterministic models: Deterministic models model the liquidity effect of a forward-looking or historical-based scenario that has been developed by the institution. An example of such a model is the development of hypothetical liquidity stress scenarios.

•Monte Carlo simulation: This statistical technique is based on simulation modeling and applies to assessing the liquidity risk done by stress testing specified variables over a future time frame.

Stochastic techniques that depend on observations of the historical volatility of cash flow variables, either using the historical statistical models such as CFaR or Monte Carlo simulation techniques that depend on historical observations of volatility, are less favourable in times of financial crisis.

Deterministic scenarios are the most effective tools for assessing liquidity risk since liquidity stress is an extreme “tail event.” The disadvantage of stochastic approaches is their incapability to accurately predict the management countermeasures that would occur during a liquidity crisis event.

Scenario Analysis: Establishing a specific and detailed description of the business and market events related to each scenario provides the basis for development of stress testing with early warning indicators in contingency funding plans. A good scenario description should include:

1. The overall level of stress due to market, economic, and credit conditions.

2. Conditions secured and unsecured wholesale funding markets.

3. Changes in counterparty haircut necessities by collateral type.

4. Liquidity effects on securities in the liquidity buffer and other assets when selling.

5. Credit grade downgrade.

6. Deposit runoff assumptions based on product and customer type, considering other factors such as insurance coverage.

7. Description of impacts on specific counterparty relationships.

8. Assessment of trigger effects on derivative margin and collateral calls.

9. Effects of regulatory actions and limit breach in jurisdictions overseas.

10. Drawdowns assumed on unfunded credit and liquidity facilities.

11. The assumed debt calls and buybacks.

12. Wholesale funding outflow-no rollover.

13. Secured funding loss-loss of repo capacity & widening of haircuts.

14. Collateral outflow scenario based on multi-notch bank downgrade.

15. Loss of secured funding-loss of access to AB funding facilities.

16. Adverse derivative cash flows- increased derivatives margin due to increased market volatility of underlying positions.

17. Credit and liquidity facilities-accelerated drawdown of credit and liquidity facilities by Customers and counterparties.

18. Deposit runoff of demand deposit.

19. Reduced investment portfolio liquidity-increased liquidity haircuts or reduced valuations of liquidity portfolio securities.

20. Rating downgrade- collateral or other liquidity impacts due to rating triggers.

21. Derivatives cash flow- increased collateral calls due to reduction in collateral value.

22. Loss of wholesale funding- early termination of unsecured wholesale funding credit lines or early redemption of wholesale fundings.

23. Deposit runoff of term deposit- exercise early withdrawal rights.

24. Loss of secured funding- loss of willing counterparties for secured funding.

25. Loss of secured funding- limitation of security types available for secured funding.