Overview of Treasury

Treasury refers to the financial department or division within a government or organization responsible for managing and controlling financial resources, including funds, assets, investments and disinvestments. Treasury plays a critical role in budgeting, cash management, and ensuring the financial stability and liquidity of the entity it serves. Treasury in a Bank is probably one of the most important departments in a Bank. It is involved with Treasury and hedge accounting, Portfolio management, Cash flow and risk modeling, multi-lateral netting and margining, GL reconciliation and FX and interest rate tracking.

Profit Centres of Treasury

Treasury consists of Front Office, Mid Office and Back Office. Normally, a Bank Treasury Front Office has the following Desks/Profit Centres:

- Fixed Income Desk: involved in buying and selling interest bearing securities, T Bills, Government Securities, Bonds, Debentures and so on.

- Money Market Desk: involved in Call Money and short-term deposits.

- Foreign Exchange Desk: involved in buying and selling currencies on Cash, Tom, Spot basis in Cash Market and Forward Market.

- Capital Markets or Equities Desk: involved in buying and selling shares in different stock exchanges.

- Derivatives Desk: involved in trading derivatives, Swaps, Options and so on and complex CDS instruments.

- Commodity Trading or Bullion Desk: involved in Gold, Silver, energy, power and metals trading and other commodities.

- Proprietary Trading Desk: involved in trading activities for the bank’s own account and capital. Asset liability management (ALM) Desk: involved in managing the risk of interest rate mismatch and liquidity and a Transfer pricing or Pooling function that prices liquidity for business lines (the liability and asset sales teams) within the bank. It centrally manages the funding requirements of the entire bank in lieu of having each division fund its own balance sheet.

Treasury Mid Office deals with MIS & Risk and Back Office is concerned with deal confirmation , settlement and funds transfer.

Divisions in Treasury in a Bank

1. Front Office

The front office is the bank’s interface with the market and clients. The front office coordinates and handles all the needs of the bank and its clients with respect to hedging and financing. Dealing room is the provider of sales, trading, structuring and advisory services, encompassing the full spectrum of Foreign Exchange, Fixed Income, Interest Rate products, Money market products and complex Derivatives Products to corporate, high net-worth individuals, money managers, pension funds, endowments, financial institutions, and governments. They provide their clients with ideas and market insights, trading services, analytics, and new products across a broad spectrum of asset classes, their local relationships, and broad global capabilities; all with the goal of enabling their clients to maximize their performance.

Front office includes the following roles:

a. Salespeople

b. Dealers

c. Corporate Finance Bankers

d. Analysts

2. Middle Office

Middle office workers are an integral part of Treasury. Mid Office becomes a Treasury core associate to manage relationships in inter-company and intra-company, leveraging multiple core stakeholders. The functions of Treasury Mid office are given below:

- Examine the roles of the key treasury departments – front office, middle office, and treasury operations

- Understand the deal life cycle for key instruments from initiation to post-settlement reconciliation

- Analysis & production and reporting of daily P & L and B/S for all Treasury relationships and products and commentary on key drivers of P&L by attribution.

- Reconcile P&L for a variety of cash and derivative instruments

- Discussion of daily P&L with the trading desk and obtaining their sign off on a daily basis.

- Interpret the risk mandate of a bank treasury

- Apply best practice techniques for mitigating market, credit, and operational risk management

- Appreciate the importance of sound liquidity management

- Examine VaR, stress testing, and scenario analysis

- Monitor and control risk limits

- Monitor and report credit exposures and excesses

- Understand best practices for the documentation of treasury transactions

- Complete and assist in analysis of the business and downstream reporting.

- Support ad hoc requests from the trading desk and infrastructure groups.

- Costs calculation, analysis and reporting of allocations of cross business funding and other charges.

- Review of balance sheet and explaining key drivers for month on month moves.

- Continuous identification and elimination of inefficiencies in the existing processes.

- Provide support and cover for other team members.

- Verify that legal documents with external parties are optimally structured.

- Making sure that the Bank follows Compliance (on the right side of compliance law)

3. Back OfficeBack office includes all process-orientated roles. An efficient back office is vital to treasury survival. It is also called Treasury Operations. Back Office function includes:

- Pre Confirmation with counter-party

- Confirmation of transactions with clients for all FX, DX, MM, CP and CM & Fixed Deposits.

- Checking all the details in the Deal Ticket and Settlement Systems

- Reconciliation of all mismatches

- Checking & preparing all statements

- Send out regular statements to Clients

- Maintaining and updating the books of entry for all assets and liability

- Posting all GL/Accounting entries for all transactions.

- Reconcile all Custodian positions

- Generation of Adhoc and Regulatory Reports

- Transfer of funds to counterparty

- Interaction with Clients for Client Relationship

- Interaction with Regulators

- Keeping track of all receivables and payables

- Verification and Account opening

- Account Closure and deletion

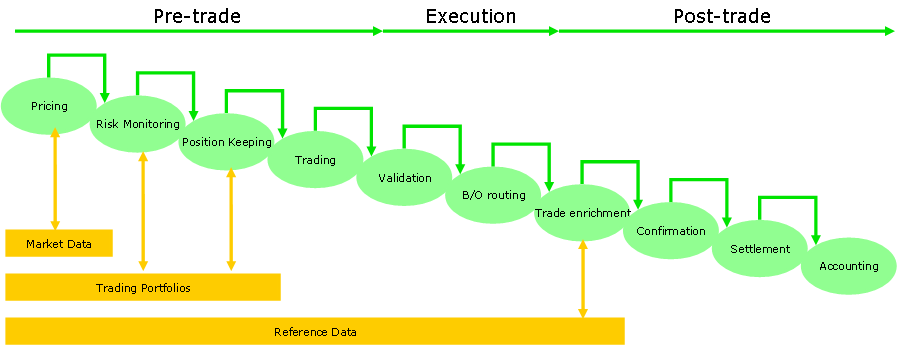

E2E Trade Flow in Treasury in a Bank

Products Traded in Treasury of a Bank

- Treasury Bills are short-term government securities with maturities ranging from a 14 Days, 91 Days, 182 Days and 364 Days in India. Bills are sold at a discount from their face value and mature at the face value.

- Treasury Notes are government securities that are issued with maturities of 2, 3, 5, 7, and 10 years and pay interest every six months.

- Treasury Bonds pay interest every six months and mature in 30 years.

- Treasury Inflation-Protected Securities (TIPS) are marketable securities whose principal is adjusted by changes in the Consumer Price Index. TIPS pay interest every six months and are issued with maturities of 5, 10, and 30 years.

- I Savings Bonds are a low-risk savings product that earn interest while protecting you from inflation. Sold at face value.

- EE/E Savings Bonds are a secure savings product that pay interest based on current market rates for up to 30 years. Electronic EE Savings Bonds are sold at face value in Treasury Direct.

- FX products: During trading hours corporate dealers are able to offer information about exchange rates and expectations and clients have the option to fix the exchange rates. Rates are based on actual market rates. In case of a disadvantageous rate the client can give the dealer, at the given moment, an “order” at what rate he is to buy or sell the mentioned currency (take profit). Meanwhile to protect clients against possible negative trends of exchange rates on foreign exchange markets clients have the opportunity together with the order “take profit” also to give the order “stop loss”, which protects them against negative market trends.

- Spot FX transactions: Spot FX transactions are available for those clients who benefit from approved spot limits. These transactions may be realised for certain minimum amount say, USD 50,000 or equivalent. The rates are based on current market rates and agreed with corporate dealers. If a spot limit is available, cash cover is not necessary on the date of trading.

- Forward transactions: Forward transactions are intended for clients who want to fix a favourable current exchange rate for the future. The client can conclude a deal with maturity on an exact day in the future or conclude “forward with floating maturity” for an agreed time frame within which the client has the opportunity to realise the contract on an optional day. In case the client wants to fix the exchange rate without delivery of assets (e.g. does not have an opened account), there is the possibility to conclude a “non-delivery forward” (NDF), which means that on maturity day there is only mutual compensation of the difference between the agreed forward price and the actual price on the market. The client can effectively change the maturity of concluded forward transaction with FX Swaps transaction.

- FX Swaps: FX swaps represent a simple type of currency swap, where one currency is exchanged for another for an agreed time period. For this type of swap the real cash flow is at the beginning and at the end of the transactions. This is utilised especially by those clients that have at their disposal financial means in currency “A” but their cash flow is in currency “B”. The advantage of FX swaps is mainly in the minimising of the costs of foreign conversion while client is protected against exchange rate risk. Another advantage of this product is the possibility to agree the transactions for an optional period and even shorten/prolong the existing swap according to the client’s requirements.

- Currency Options: All types of options and their combinations for the purpose of creating a variety of structures respecting the client’s need. The options, as in case of the other offered products of the foreign exchange market, can be concluded in FCY/FCY or FCY/EUR

- Term Deposits: Term deposits may be denominated in LCY/FCY. Maturities from overnight up to 1 year are available (on a case-to-case basis longer maturities are considered as well). Term deposit rates are based on current money market rates. There is a minimum amount per transaction. The basis for interest calculation is actual/360 or Actual/Actual.

- Corporate Bonds and Commercial Papers: Corporate bonds and Commercial Papers are another alternative to term deposits.

- Promissory Notes: Promissory notes issued by Bank are alternative investment instruments for clients.

- Forward-Forward: Forward-Forward represents an agreement on interest rates for setting up a deposit/loan that starts in the future. It enables the client to hedge against a decrease in the interest rate (deposit) or increase of interest rate (loan).

- FRA: FRA, unlike Forward-Forward, represents an off – balance sheet instrument where the difference of the agreed rate and actual reference rate is compensated at the beginning of the agreed period. The advantage of FRA is the existence of an interbank (FRA) market and as a result, a higher liquidity of this product.

- Interest Rate Swaps: Interest swaps represent the exchange of interest rates, most frequently a fixed interest rate for floating in the same currency, while the principal is not exchanged. The advantage is that it offers a relatively simple and flexible structure.

- Currency Swaps: Currency swaps offer besides hedging against movement of exchange rates (FX swap) also hedging against interest risk. There are many variations of currency swaps where the principal can be exchanged/or not exchanged at the beginning/at the end of the period, exchange rates can be agreed as fixed towards the fixed rate, floating towards floating, or floating towards fixed rate. Currency swap transactions are concluded for a long-term period and a high volume with ensured high liquidity. Swaps can be concluded for FCY/FCY as well as FCY/LCY.

- Interest Options: Bank, as in the case of currency options, offers a complete range of interest options. The basic types are CAP options where the buyer (debtor) of the option hedges against the increase of the interest rate while profiting from the decrease of the interest rate, and FLOOR options where the buyer (creditor) of the option hedges against the decrease of the interest rate while profiting from the increase of the interest rate.

Difference in Derivatives Products Traded in Treasury of a Bank

Differences Between Futures and Forwards

1.Futures are standard instruments, governed by Stock Exchanges rules and regulations, size, amount, settlement date while Forwards are traded OTC between two parties & determined by private parties and varies from contract to contract.

2.Futures normally do not have Credit Risk as they are settled through Exchange’s Clearing House where Daily mark-to-market and margining are automatically required while Forwards carry both Credit Risk and Market Risk.

3.Futures are settled at the settlement price fixed on the last trading date of the contract (i.e. at the end). Forwards are settled at the Forward price agreed on at the trade date (i.e. at the start).

4.Futures are generally subject to a single regulatory regime in one jurisdiction, while forwards – although usually transacted by regulated firms – are transacted across jurisdictional boundaries and are primarily governed by the contractual relations between the parties.

Difference between options and futures

1. An option gives the buyer the right, but not the obligation to buy (or sell) a certain asset at a specific price at any time during the life of the contract. A futures contract gives the buyer the obligation to purchase a specific asset, and the seller to sell and deliver that asset at a specific future date, unless the holder’s position is closed prior to expiration.

2.No upfront cost needs to be paid in Futures whereas buying an Options position does require the upfront payment of a premium by Buyer to Seller.

3.Generally, the underlying position is much larger for Futures contracts, and the obligation to buy or sell this certain amount at a given price makes futures more risky for the inexperienced investor.

4.The final major difference between these two financial instruments is the way the gains are received by the parties. The gain on a option can be realized by exercising the option when it is deep in the money, going to the market and taking the opposite position or waiting until expiry and collecting the difference between the asset price and the Strike Price. In contrast, gains on futures positions are automatically ‘marked to market’ daily, meaning the change in the value of the positions is attributed to the futures accounts of the parties at the end of every trading day – but a futures contract holder can realize gains also by going to the market and taking the opposite position.

Risk Management by Treasury

FX Risk: It entails the chance of significant exchange value fluctuation between the currency of an enterprise’s home country and a foreign currency or between two foreign currencies, including the complete devaluation of any currency which can result in the full loss of the investment, as well as the chance of unlimited loss of the FX product.

Interest Rate Risk: It originates due to the changes of the interest rates of the currencies which influence the value or payment of the transaction. It can happen on the date of maturity or during the whole life of the product and can affect the payments and the value of the transaction. IR risk may include the full devaluation of the treasury deal, its significant value change during the term, including in certain cases the chance of unlimited loss where an open transaction is closed during its term. Changes in the central bank base rate, changes in interbank reference interest rates (e.g.: BUBOR,EURIBOR, LIBOR) or Yield curve shifts or changes in its incline create interest rate risk.

Liquidity Risk: A financial product is liquid if it can be converted to cash easily, at a freely chosen date, in relatively short time, avoiding value loss and keeping transaction costs low. Market liquidity risk is also a threat of a market position being impossible to close successfully in a short time at market price, only at less favourable market rate, so realising a satisfactory market price demands maintaining the position, which may necessitate the borrowing of liquid assets, thereby making the management of financing liquidity risk more difficult.

Volatility Risk: Volatility is the degree of variation of a trading price series over time. The bigger the financial instrument’s price fluctuation is, the riskier an investment / instrument can be considered, so volatility can be used to characterise how risky a particular product is. Volatility and its change can have a significant impact on options’ price/value, so subject to different volatility the value of an option can show substantial differences at different times.

Commodity Price Risk: Commodity risk entails the chance of significant shifts in the prices of raw materials required for an enterprise to operate with and manufacture or such as the enterprise may produce. If a treasury transaction is executed to mitigate the underlying commodity exposure, this threat is reduced to a large extent. However, the chance of large losses cannot be ruled out even if a deal is concluded purely for purposes since different external, economic, social and political factors also affect the operation of the enterprise, and it also has to face unique risks.

Inflationary Risk: An important type of macroeconomic risk that has a direct impact on the value of investments’ real return. The real return on investments with nominally fixed yields is principally determined by inflation changes. Inflation has an impact on all financial instruments.

Country Risk: This is another important type of macroeconomic risks. It refers to the threat of a country’s economic stakeholders being unable or unwilling to settle their payment obligations due to political/economic events or administrative restrictions, and investors suffer losses. International credit rating agencies’ ratings can serve as guidance in terms of national and local policy and regulations related risks.

Issuer Risk: A type of credit risk that relates to securities investments. In case the security issuer becomes insolvent or declares bankruptcy, it is possible that the security holder will not receive the invested principal and any interest or return on it, or only receive a part of those.

Partner Risk: a type of credit risk where an enterprise suffers losses on the settlement of a transaction because of the counterparty’s potential non-fulfilment (liquidation, bankruptcy.).

Operational Risk: By operational risk, we mean the chance of loss derived from the inappropriate planning of external/internal processes or their bad execution, the malfunction of technical equipment in use, natural disasters, human errors or intentional fraud.

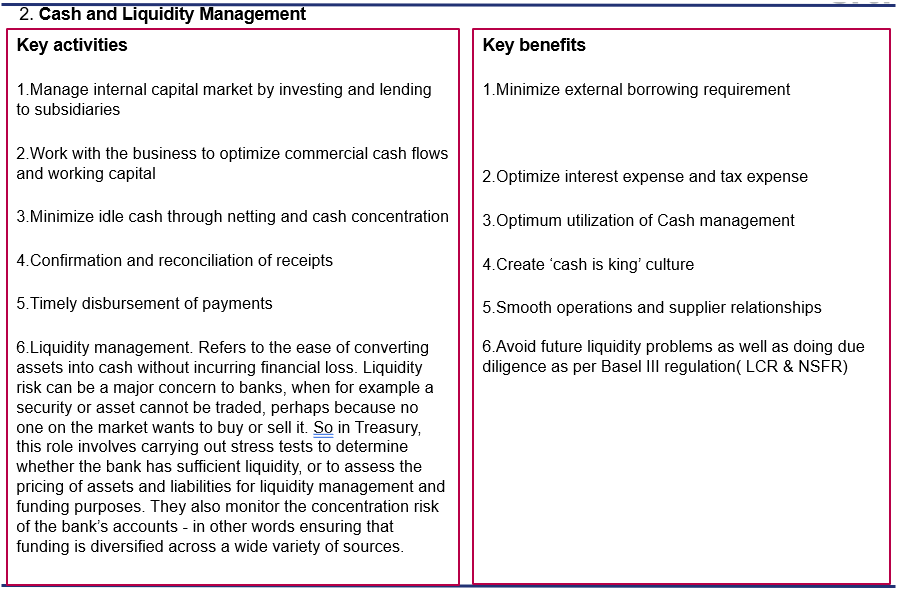

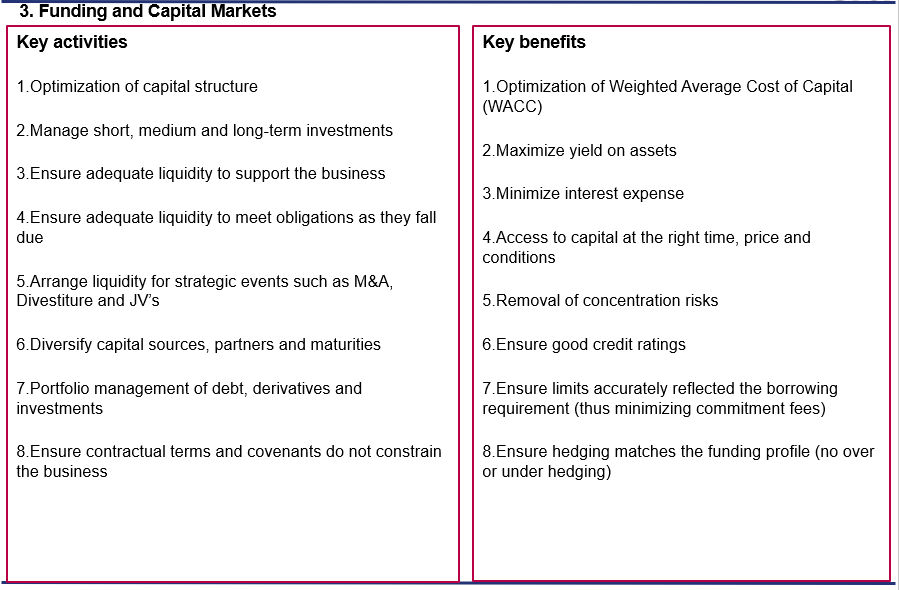

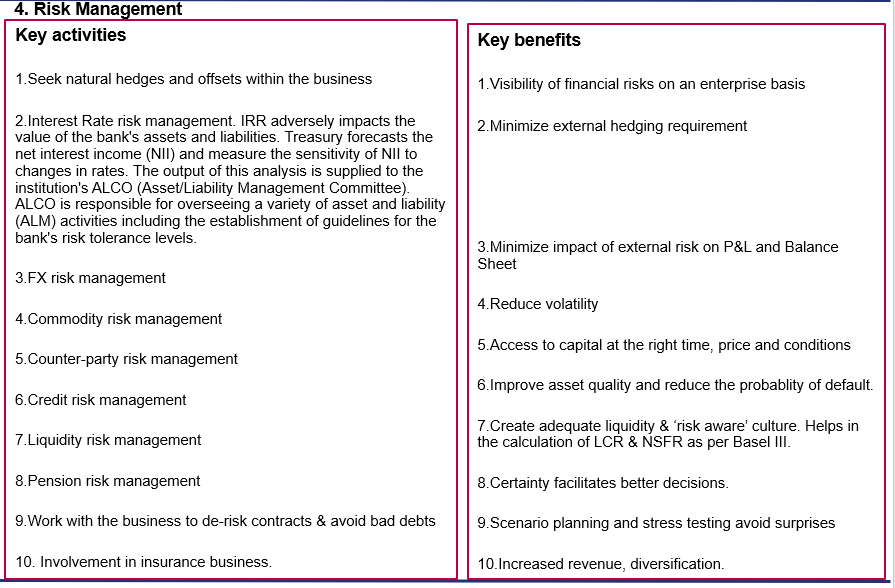

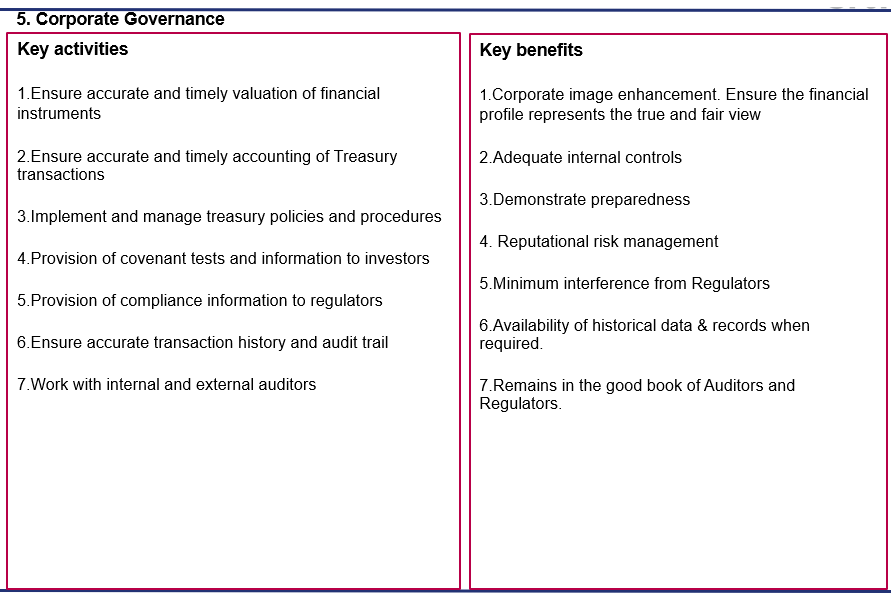

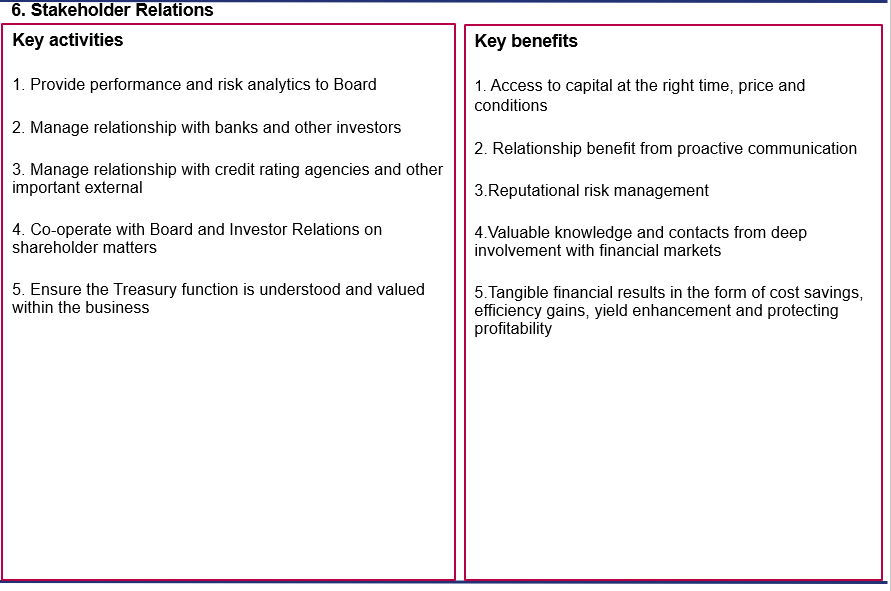

Treasury Functions in a Bank

Treasury function undertakes a range of complex and skilled tasks; liaises with internal and external stakeholders and plays a key role in the smooth functioning and value creation of an organization. It manages the following risks:

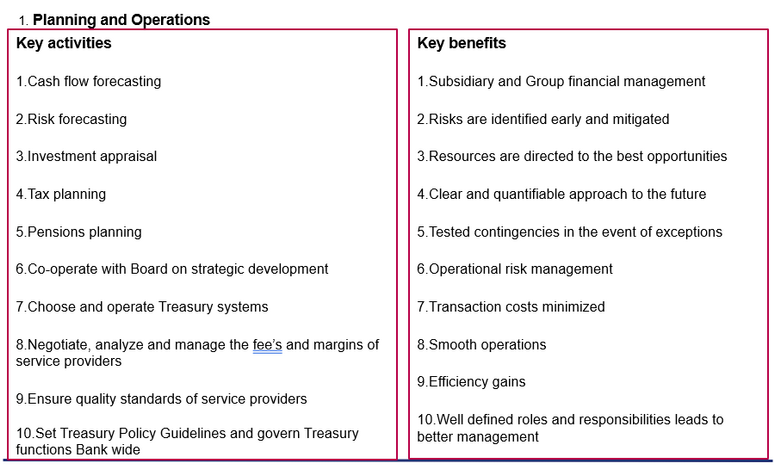

Although the role of the Treasury function is constantly evolving, it can be broken down into 6 broad but interlinked categories:

The Greeks …Risk Metrics

The Greeks are vital tools in risk management. Each Greek measures the sensitivity of the market value of an Asset or Portfolio to a small change in a given underlying parameter, so that component risks may be treated in isolation and the portfolio can be rebalanced accordingly to achieve a desired exposure and return.

They are called the Greeks because four out of the five are named after letters of the Greek alphabet. Vega is the exception. For reasons unknown, it is named after the brightest star in the constellation Lyra. At times, Vega has been called Kappa, but the name Vega is now well established. Four of the five are Risk metrics. Theta is not because the passage of time is certain – it entails no risk. Theta is akin to the accrual of interest on a bond.

Delta (Δ): The delta of an option is the rate of change in the value of the option with respect to change in the price of the underlying assets of the option. It is the first order sensitivity.

Rho (ρ): Rho of an option is the rate of change in the value of an option with respect to change in the level of interest rates.

Theta (θ): The theta of an option is the rate of change in the value of the option with respect to passage of time, with all else remaining the same. It is also called the “time decay” of the option.

Vega (ν): The Vega of an option is the rate of change in the value of the option with respect to volatility of the underlying assets of the option.

Gamma (Г): The gamma of an option is the rate of change of the option’s delta with respect to the change in the price of the underlying assets of the option.

Application of AI in Bank Treasury

AI in Bank Treasury is transforming how financial institutions manage liquidity, risk, investments and regulatory compliance. AI enhances decision-making, automates processes, reduces operational risks and improves forecasting accuracy. Early adopters gain a competitive edge in liquidity optimization, risk mitigation and automated decision-making. AI is being used in following areas:

1. Liquidity Management & Cash Flow Forecasting

- AI models analyse historical transaction data, customer behaviour and macroeconomic indicators to predict cash flows more accurately.

- Real-time liquidity monitoring helps treasurers optimize funding and reduce idle balances or overdraft costs.

- Machine Learning (ML) helps optimize intraday liquidity and reduce dependency on costly short-term funding.

- Example: J.P. Morgan’s Cash Flow Intelligence improves liquidity forecasting, using AI tools.

2. Risk Management (Market, Credit, & Operational Risk)

- Credit Risk: AI assesses counterparty credit risk using behavioural, market, and credit bureau data. Predictive models assess counterparty credit risk by analyzing real-time financial data.

- Market Risk: Neural Networks forecast interest rate movements, FX volatility, and asset price fluctuations.

- Stress Testing & Scenario Analysis: AI simulates complex what-if scenarios under extreme market conditions faster than traditional tools. Reinforcement Learning (RL) helps simulate market shocks for stress testing.

- Example: Banks use AI-driven VaR (Value at Risk) models for real-time risk assessment.

3. Fraud Detection and Compliance

- Detects unusual transaction patterns or breaches in treasury limits in real time.

- NLP tools automate monitoring of regulatory updates, flagging compliance risks.

- AI ensures KYC/AML standards are met by screening counterparties and payments efficiently.

- Example: HSBC partnered with Quantexa to build an AI-based Financial Crime Detection Platform using graph analytics and machine learning.

4. Algorithmic Trading

- AI-powered high-frequency trading (HFT) systems execute trades at optimal prices using NLP (news sentiment analysis) and deep learning.

- Reduced market impact and trading costs for clients. Models based on Sentiment Analysis, news feeds, and market depth predict short-term price movements.

- Example: JPMorgan Chase developed an AI-based execution algorithm called LOXM (short for “Liquidity Optimizer”) for its Equity and FX trading desks.

5. Investment and Portfolio Optimization

- AI helps optimize treasury portfolios by balancing yield, duration, liquidity, and risk.

- Reinforcement Learning and predictive analytics guide dynamic reallocation strategies in response to market changes.

- Reinforcement Learning optimizes bond portfolio management by predicting yield curve movements.

- Example: Goldman Sachs’ Marcus uses AI for automated investment strategies.

6. Interest Rate & FX Risk Hedging

- AI models predict interest rate movements using central bank communications (NLP-based sentiment analysis).

- Machine Learning algorithms optimize FX hedging strategies by analyzing historical volatility and correlations.

- Example: Bank of America uses AI and advanced analytics to improve hedging strategies for Interest Rate Risk in its asset-liability portfolio and FX Risk from multinational clients and proprietary trading positions.

7. Regulatory Compliance (Basel III/IV, AML, etc.)

- AI automates Anti-Money Laundering (AML) checks by detecting suspicious transactions.

- NLP helps analyse regulatory texts (e.g., MiFID II, Dodd-Frank) to ensure compliance.

- Example: HSBC uses AI-based transaction monitoring to reduce false positives in AML alerts.

8. Balance Sheet Optimization

- AI models recommend optimal funding structures (e.g., deposits vs. wholesale funding).

- ML helps in asset-liability management (ALM) by forecasting deposit behaviours.

- Example: Wells Fargo applies AI and machine learning to optimize its Net Interest Margin by analysing loan and deposit pricing strategies, interest rate scenarios, customer behaviour and sensitivity and balance sheet structure and liquidity buffers.

9. Cybersecurity & Payment Fraud Detection

- AI detects real-time payment fraud using anomaly detection algorithms.

- Behavioural biometrics (keystroke dynamics, mouse movements) enhance security.

- Example: Mastercard’s AI-powered fraud detection reduces false declines.

10. Forecasting and Predictive Analytics

- Predict interest rate trends, inflation, and currency exchange movements to support strategic ALM.

- AI can improve FTP (Funds Transfer Pricing) by predicting internal fund demand and costs.

- Example: Barclays is using AI based predictive analytics to understand customer churn and upsell opportunities.

11. Robotic Process Automation (RPA) in Treasury Operations

- Automates repetitive tasks like report generation, reconciliation, confirmations, and data entry.

- Reduces manual errors and frees up human resources for strategic work.

- Example: Deutsche Bank implemented RPA as part of its treasury transformation strategy to automate operational tasks, improve controls, and enhance the efficiency of cash and liquidity management.

12. Treasury Chatbots and Digital Assistants

- AI-powered assistants answer queries related to FX rates, cash positions, interest accruals, and generate reports on demand.

- Useful for real-time updates during trading hours and decision support.

- Personalized cash management solutions using predictive analytics.

- Example: Bank of America’s Erica assist corporate clients in treasury queries.

Challenges in AI Adoption for Treasury

While AI offers significant benefits in automating and optimizing treasury operations, it faces several challenges in its implementation and adoption. Treasury functions are complex, regulated, and data-intensive – making integration of AI a strategic, technical, and operational hurdle.

1. Data Quality and Integration Issues

- Treasury data often resides in silos across ERP, trading platforms, risk systems, and external sources.

- Inconsistent formats, missing historical data and low granularity hinder AI model training.

- Real-time data ingestion from multiple sources (FX rates, interest curves, liquidity positions) is complex. Inaccurate or delayed trade confirmations can mislead predictive liquidity models.

2. Model Interpretability and Trust

- Treasury Traders and Regulators demand explainable AI, especially in risk management and hedging.

- Complex models (neural networks) are often black boxes, making it hard to validate decisions.

- Lack of model governance and transparency delays adoption. Regulators question an AI’s decision on hedge execution without a clear logic trail.

3. Regulatory and Compliance Concerns

- AI must comply with Basel III/IV, IFRS 9, BCBS 239 and local treasury regulations.

- Fear of non-compliance due to autonomous AI decisions (liquidity forecasting or FTP mispricing).

- Regulatory bodies still developing guidelines for AI governance in banking.

4. High Implementation Costs and ROI Uncertainty

- Building, training, testing, and integrating AI into existing treasury infrastructure is costly.

- ROI is often delayed or hard to measure – especially for predictive or risk-averse treasury functions.

- Legacy system constraints increase integration costs.

5. Talent and Skill Gaps

- Treasury teams typically lack AI expertise.

- Cross-functional collaboration between Treasury, IT, risk, and AI teams is needed but often siloed.

- Resistance from staff fearing job loss, job displacement or loss of control over critical functions.

6. Cybersecurity and Data Privacy Risks

- AI tools that connect to real-time market feeds, ERP systems, and bank accounts increase the attack surface.

- Treasury often handles sensitive transaction and funding data; model breaches could result in severe losses.

- Cybersecurity Risks (AI models can be targets for adversarial attacks).

7. Scalability and Customization Challenges

- AI models need to scale across currencies, jurisdictions, legal entities, and products.

- Off-the-shelf AI tools often need heavy customization for bank-specific treasury policies and hedging strategies.

8. Lack of Standardized Frameworks and Benchmarks

- No universal benchmarks or performance KPIs for AI in treasury operations.

- Hard to compare model effectiveness across banks or evaluate vendor solutions.

Future Trends of AI in Banking

AI is rapidly evolving, and its applications in banking are expanding beyond automation into predictive analytics, hyper-personalization, and autonomous decision-making. Banks that invest in Explainable AI, Quantum AI, and Synthetic Data will lead the next wave of financial innovation.

1. Hyper-Personalization of Banking Services with Generative AI

- AI will deliver real-time, context-aware recommendations for products (loans, credit cards, investments).

- Banks will use behavioural analytics to tailor offers at the micro-segment or even individual level.

- Generative AI will power virtual financial advisors, offering real-time investment advice.

- Example: Banks may use AI avatars for 24/7 customer interactions with human-like responses.

2. AI and Quantum Computing for Risk Modeling & Fraud Detection

- Quantum computing + AI will enable instant risk simulations, optimizing portfolios in microseconds.

- Fraud detection will improve with quantum-enhanced anomaly detection, reducing false positives.

- Example: JPMorgan and Goldman Sachs are already experimenting with quantum machine learning.

3. AI & Blockchain Convergence for Smart Contracts & Decentralized Finance

- AI will automate DeFi (Decentralized Finance) strategies (e.g., yield farming, liquidity provisioning).

- Smart contracts will self-adjust based on AI-driven market signals.

- Crypto portfolio management for clients

- Example: AI-managed stablecoins that dynamically rebalance reserves.

4. Explainable AI (XAI) for Compliance & Trust

- Regulators will demand transparency in AI decision-making.

- XAI techniques (SHAP, LIME) will help banks justify AI-driven credit scoring, trading, and risk models.

- Example: AI audit trails for Basel IV compliance to prove model fairness.

5. AI-Powered Central Bank Digital Currencies (CBDCs)

- Smart CBDCs will use AI to automate monetary policy execution (e.g., dynamic interest rates based on real-time inflation data).

- Programmable money (AI-controlled smart contracts) could optimize liquidity distribution.

- Example: China’s digital yuan (e-CNY) may integrate AI for fraud prevention.

6. Embedded AI in Banking-as-a-Service (BaaS)

- Non-banks (Fintechs, E-Commerce platforms) will embed AI-driven banking services.

- Example: Shopify offering AI-powered cash flow forecasting for merchants.

7. Cognitive Banking

- Beyond transactions, banks will understand emotions, intentions, and motivations using cognitive AI.

- Behavioural biometrics, sentiment analysis, and neuro-linguistic cues will be integrated for fraud detection and customer engagement.

8. AI-Driven Regulatory Compliance (RegTech 2.0)

- Real-time compliance monitoring using NLP to scan millions of transactions for AML risks.

- AI auto-generates regulatory reports (MiFID II, Basel III).

9. Conversational AI 2.0

- Voice and chatbots will evolve into intelligent digital bankers using natural language understanding (NLU).

- These bots will handle complex queries like financial planning, dispute resolution, or regulatory guidance.

- Integration with platforms like WhatsApp, Alexa, and Google Assistant will rise.

10. AI-Driven Autonomous Finance

- AI-led decision-making in treasury, investments, and personal finance.

- Algorithms will automatically manage savings, investments and debt repayments for customers.

- Example: Robo-advisors rebalancing portfolios or AI treasury bots executing real-time hedges without human intervention.

11. AI for Real-Time Risk and Compliance Monitoring

- AI will enable 24/7, real-time surveillance of transaction patterns, market movements, and regulatory shifts.

- Self-learning compliance bots will interpret changes in laws and automatically adjust internal policies.

- AI will also play a key role in climate risk, cyber risk, and operational resilience assessment.

12. AI and Open Banking Integration

- With open banking and API frameworks, AI will analyse customer data across multiple institutions.

- Enables cross-bank financial health scoring, unified cash flow predictions, and credit risk models.

13. AI-Enhanced Financial Inclusion

- AI will help onboard and underwrite credit-invisible populations using alternative data (e.g., utility bills, mobile data, social profiles).

- Enables micro-lending and micro-insurance at scale in emerging markets.

14. Synthetic Data for Training AI Models

- Banks will use AI-generated synthetic data to train fraud detection & credit risk models without exposing real customer data.

- Helps overcome data privacy laws (GDPR, CCPA) while improving model accuracy.

- Example: Mastercard’s Synthetic Data for testing fraud algorithms.

15. Continuous Authentication

- AI will analyse typing patterns, mouse movements, and voice for frictionless yet secure authentication.

- Example: HSBC’s voice recognition AI for phone banking.